Although people cannot eat gold, it attracts them as a magnet since the dawn of time. It is a universal metal in its essence. Gold was used in the monetary circulation even in the previous century, since the coins made of it didn’t become rusty. Gold is widely used as an industrial material today, one of the main features of which is a unique electrical conductivity. Apart from the traditional wide application of gold in the production of jewelry, it has often been mentioned with nanoclusters and solar batteries during the past decade of intensive development of high technologies. Gold is rather reliable and resistant to corrosion, which makes it an ideal material for a long-term use in aircraft engineering and space industry. As of now, gold is traded on public exchanges and its cost changes every minute. It makes millions of traders all over the world monitor dynamics of its price quotes. The reasons for buying and selling gold by market participants and creating its demand and supply could be completely different: speculations, buying or selling the physical metal, risk hedging or commercial use.

In this article:

-

- Demand and supply forces.

- Specifications of gold futures contracts.

- What futures contracts fit better to an intraday trader?

Demand and supply forces

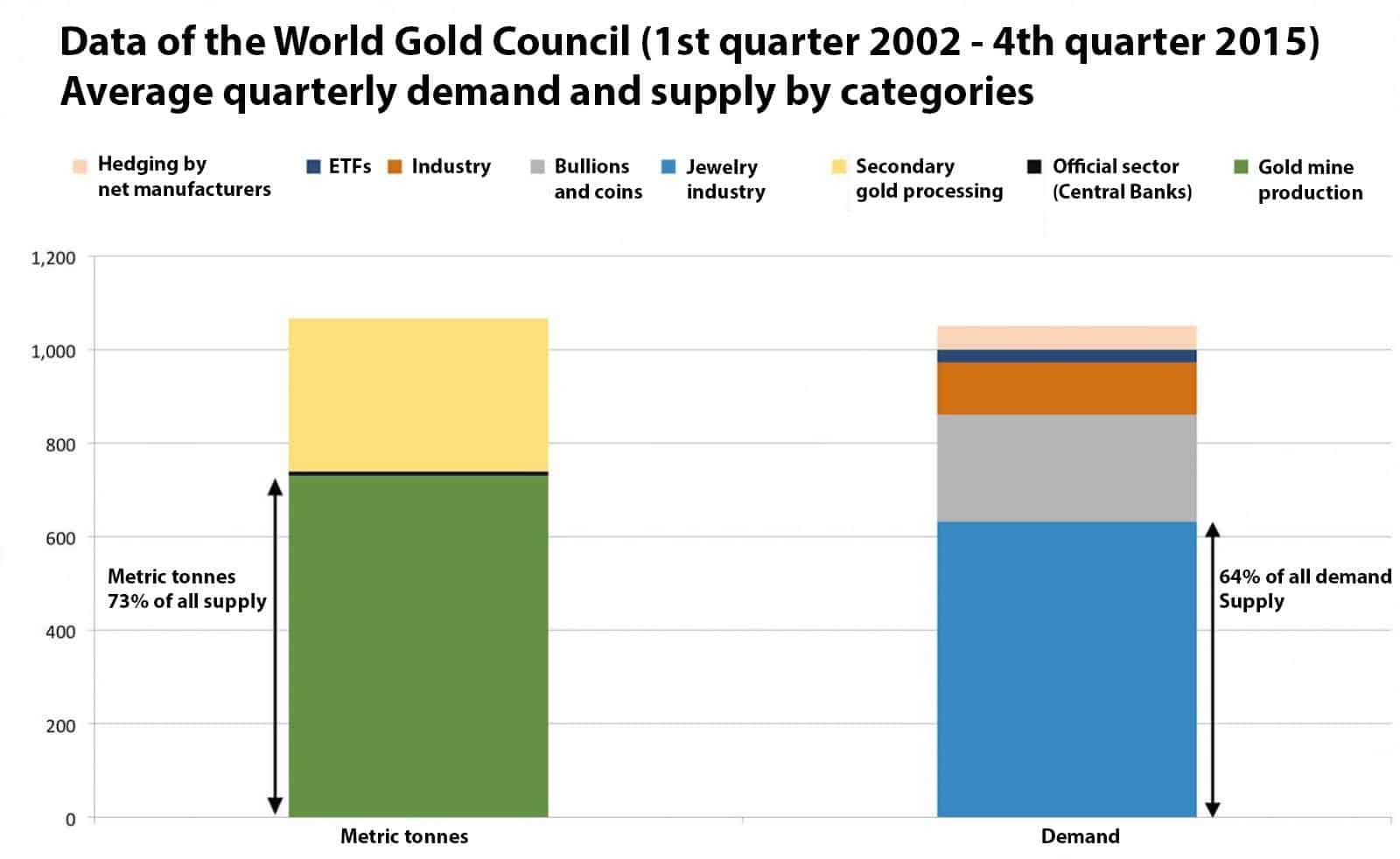

For 13 years, the major part of the gold supply comes from gold mines (73%) and major part of its demand is formed by the jewelry industry (64%). It is necessary to note that the official sector (Central Banks), net manufacturers and Exchange Traded Funds (ETF), which trade gold, also exert influence on its demand and supply, but their influence on the gold market is of the situational nature and may change every quarter. For example, only during one quarter (1st quarter of 2009) out of 52, the ETF demand for gold exceeded requirements of the jewelry industry. During the other quarters, the volumes of demand and supply of the participants of the gold market didn’t exceed the volume of supply of gold mines and requirements of the jewelry industry.

Physical demand and supply are formed by jewelry manufacturers (64%) and gold miners (73%)

(Source: BullionStar.com).

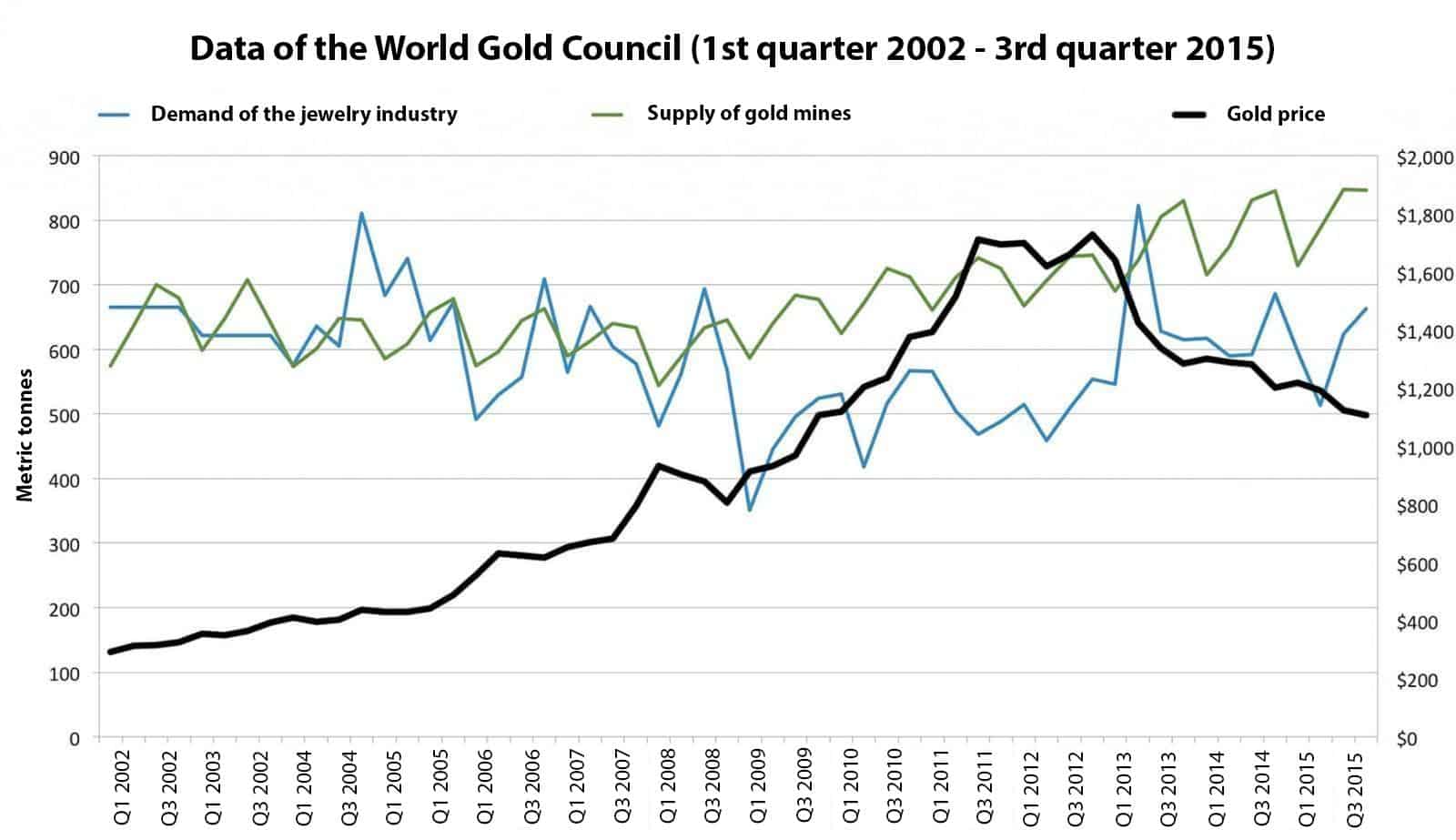

While the data of the World Gold Council on the gold physical demand and supply are comprehensive, the supply of gold mines and demand of the jewelry industry should have a direct correlation and respectively influence the gold price. However, as we can see from the chart below, it doesn’t happen.

Correlation of the middle-term and long-term gold prices with the volume of its physical demand and supply is not available (Source: BullionStar.com).

As we can see from the chart above, the demand of the jewelry industry on gold reduced and rarely grew higher than the supply of gold miners during the period of the bullish market from 2002 until 2011. Whereas, the volumes of the gold mine production grew during that period of time and the gold price grew during that period of time in six times. Do the jewelry industry demand and gold mine supply forces influence the middle-term and long-term gold price? Obviously not, however, it should be added that the correlation between the gold production and its price is still observed in the very long-term perspective since it takes more than 10 years to put a gold mine into operation.

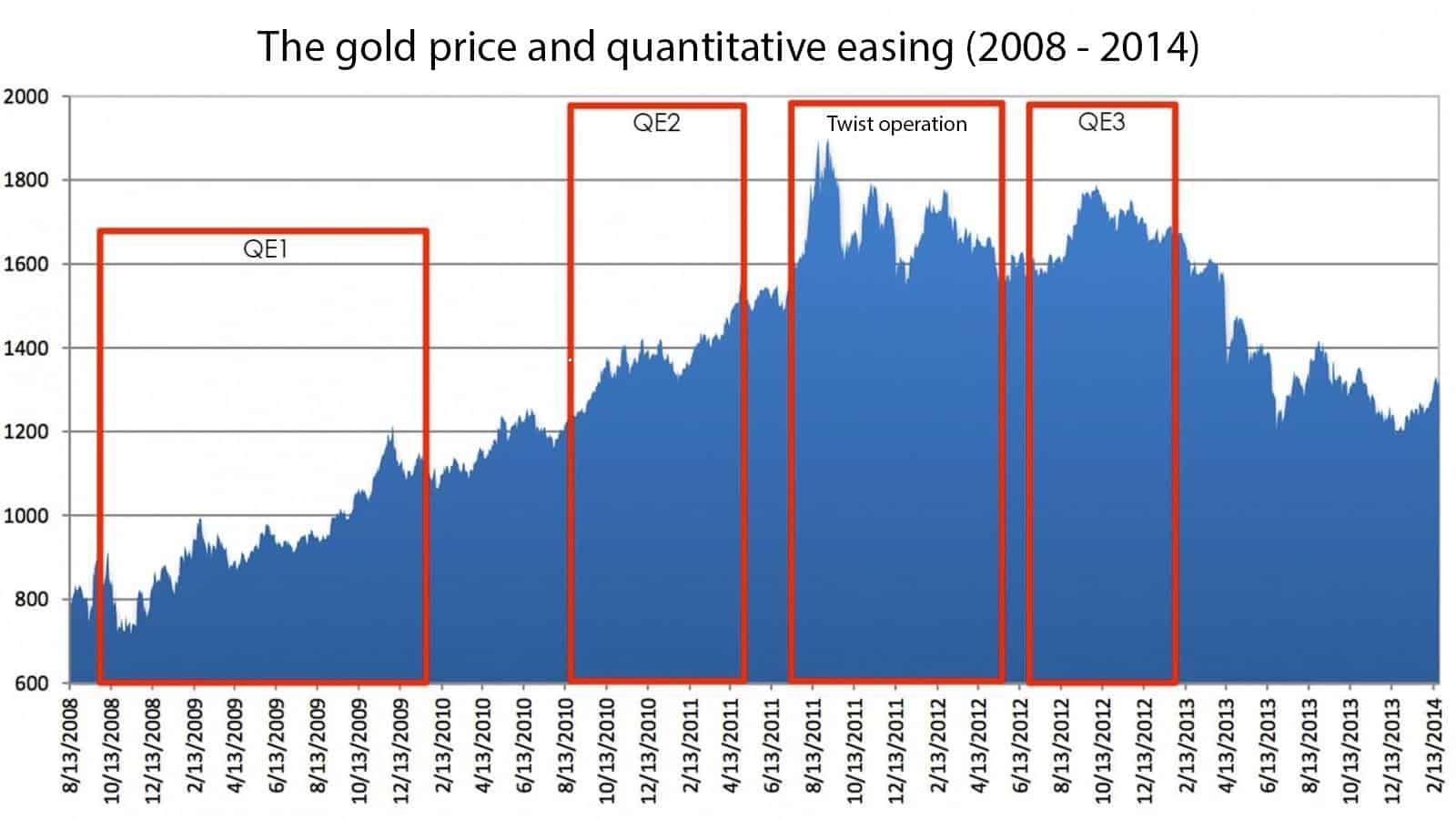

What does then exert influence on the gold price in the middle-term and long-term perspective? Note the data of the chart below. The Quantitative Easing (QE) program of the US FRS, which was launched after the economic crisis, assumed stimulation of crediting, reduction of interest rates and asset relief from the market into the FRS balance. Realization of its QE1, QE2 and QE3 stages was carried out by the US FRS just during the period from 2008 until 2014. The gold cost in the market significantly depends on the realization of the quantitative easing program and launch of its next stages. So much so that the gold price sharply fell in 2014 during one trading session against the background of the news about closing up the quantitative easing program in the US.

Correlation of the gold price with realization of the quantitative easing program of the US FRS

(Source: PGMcapital.com).

Specifications of gold futures contracts

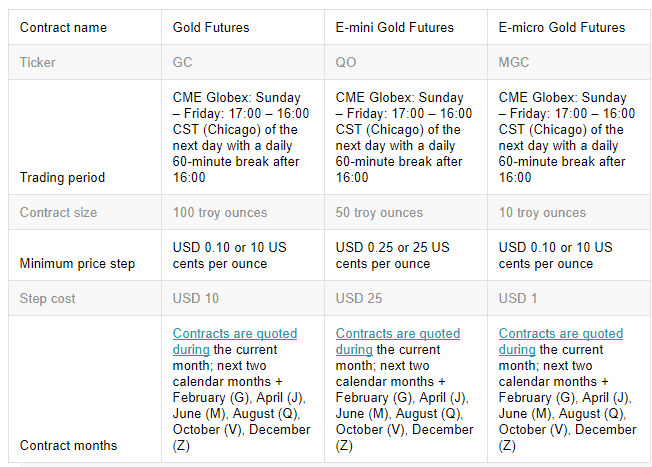

Gold futures are available in the form of standardized and regulated exchange contracts. These contracts are mainly traded on the Chicago Mercantile Exchange (CME), the London Metal Exchange (LME), the Commodity Exchange (COMEX) and the Tokyo Commodity Exchange (TOCOM).

Volumes of the gold futures contracts, traded on the London Metal Exchange, COMEX and Chicago Mercantile Exchange, are measured in troy ounces and their prices are set in USD and US cents for 1 troy ounce of gold 23.88 carat fine. Gold futures on the Tokyo Commodity Exchange are measured in kilograms and grams of gold 24 carat fine and the cost of such futures contracts are measured in JPY.

Trading is carried out during the current month; next two calendar months; any February, April, August and October within 23 months, any June and December within 72 months, starting from the current month. The contract trading stops three days before the beginning of a new contract month.

The volume of one such standard gold futures contract (ticker: GC) is 100 troy ounces (about 3.11 kilograms). Its alternatives are a settlement E-mini Gold futures (ticker: QO) with the volume of 50 ounces and a delivery E-micro Gold futures (ticker: MGC) with the volume of 10 ounces, which are traded during those months when a standard contract is traded.

The table below shows the specifications of a standard, mini and micro futures on gold.

The standard gold futures price step is only USD 0.10 or 10 US cents on the futures exchange. This step is called a ‘tick’ – a minimum futures contract price change. If you buy or sell a futures contract, your profit or loss is determined by how many ticks the price would move from the place of your entry into the market. You should know the cost of one tick to calculate the profit or loss by each traded contract.

- The tick size is USD 10 (100 troy ounces multiplied by USD 0.10) for one standard futures contract. It means that one tick of the price movement under each of such a contract would result in a profit or loss in the amount of USD 10. If the price changes by 10 ticks, you will receive or lose USD 100. If the price changes by 10 ticks and you have executed 3 futures contracts, your profit or loss would be USD 300.

- The tick size is USD 25 (100 troy ounces multiplied by USD 0.25) for one mini futures contract. It means that one tick of the price movement under each of such a contract would result in a profit or loss in the amount of USD 25. If the price changes by 10 ticks, you will receive or lose USD 250. If the price changes by 10 ticks and you have executed 3 futures contracts, your profit or loss would be USD 750.

- The tick size is USD 1 (10 troy ounces multiplied by USD 0.10) for one micro futures contract sometimes called micro-gold. It means that one tick of the price movement under each of such a contract would result in a profit or loss in the amount of USD 1. If the price changes by 10 ticks, you will receive or lose USD 10. If the price changes by 10 ticks and you have executed 3 futures contracts, your profit or loss would be USD 30.

The size of funds required for opening an intraday trading position is called an intraday or intrasession margin and its size could differ depending on a broker and could be reconsidered in the course of time.

You would need to have USD 1,000 on your trading account plus additional funds in case of losses for intraday standard gold futures contract (ticker: GC) trading.

It is assumed that you trade only during a trading session (during a day) and close all your positions every day before the session ends. If you keep your position open until the next trading session, that is you rollover your position to the next day, the initial and maintenance margin requirements are applied to you. It assumes the availability of a bigger amount on your trading account than it was required for the intrasession margin.

Margin requirements for trading gold futures are set by exchanges and could be periodically changed. These changes take place depending on the gold price fluctuations with the aim to provide an adequate collateral size on the accounts of the participants of trades. Usually, exchanges notify about the changes of their margin requirements minimum one day in advance. For example, the CME Group increased the gold futures margin requirements in September 2017. Thus, the standard futures contract maintenance margin was USD 4,450 as of December 2017.

What futures contracts fit better to an intraday trader?

Intraday gold trading is a short-term speculative trading with this precious metal. Real physical gold doesn’t take any part in this process and doesn’t pass from one futures market participant to another. All trades are executed in the electronic form and only profits or losses are reflected on the trading accounts of traders.

There are several methods of gold trading, but the basic one is trading a gold futures contract. A futures contract is an agreement binding both sides to execute a buy-sell of a commodity or another instrument in the future at a specified price. If you buy a gold futures contract, it doesn’t mean that you would become an owner of real physical gold. Intraday traders close all their futures contracts (trades) at the end of every trading day, making money on the difference of the prices of a bought and sold contract.

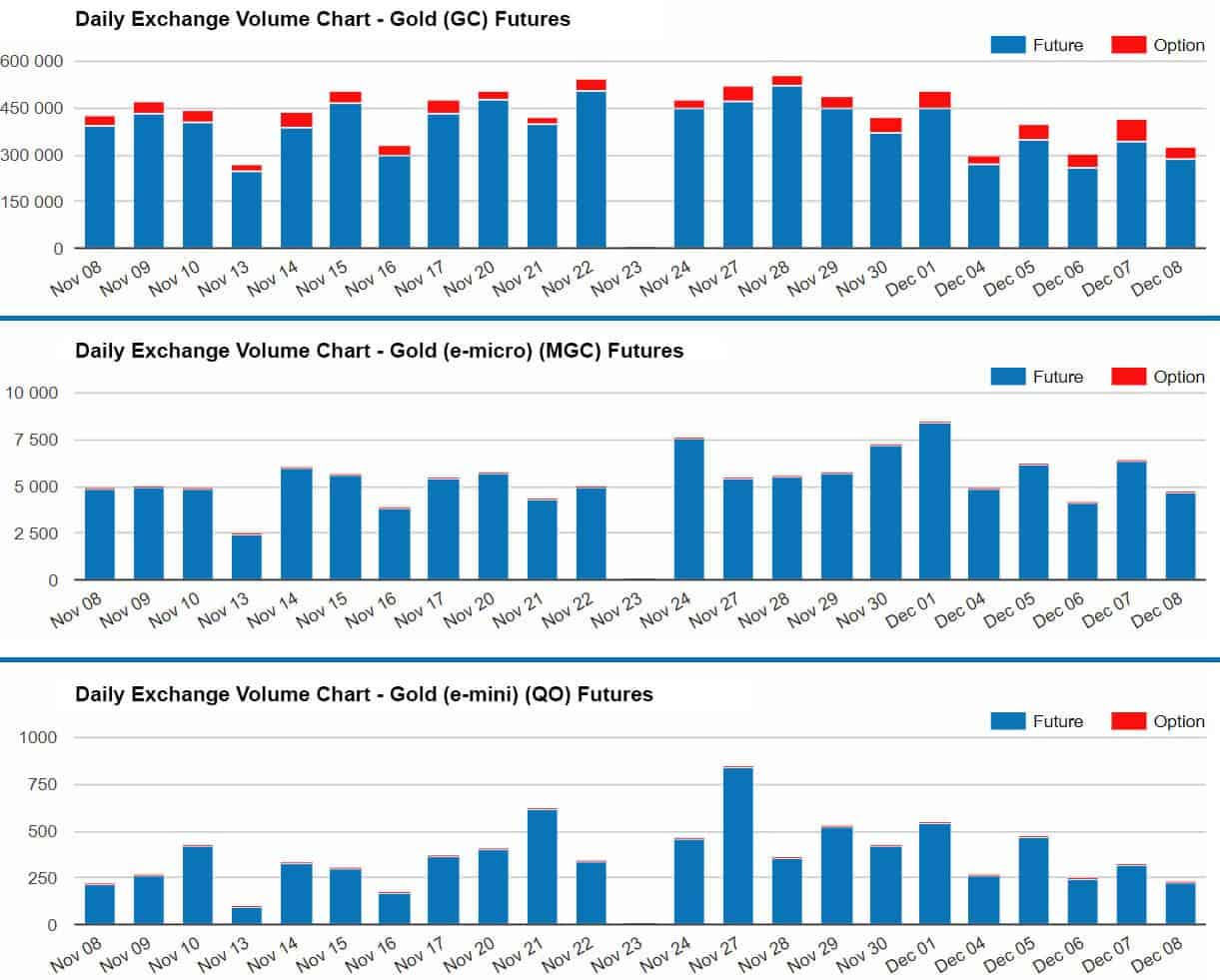

The standard type of a gold futures contract is traded (out of three main contract types) much more active from the point of view of the trading volumes and significantly exceeds the trading volumes of the micro and mini contracts.

Comparison of the day trading volumes of GC, MGC and QO futures (Source: CME Group).

The chart data tell us that the average daily volume of trading standard gold futures exceeds 250,000 contracts, while the aggregate average daily trading volume of its younger brothers is even less than 10,000.

It means for an intraday trader that standard futures contracts are a more efficient variant of trading. Liquidity, which comes with them, allows intraday traders to trade quickly in the futures market with a relevant easiness, while gold mini contracts are less liquid even if compared to micro contracts. The lower the liquidity, the more the prices are perceptive to the volume of executed trades, and this makes their intraday trading less efficient.

As we already wrote in the Top 9 most liquid CME futures. Part 2 article, the standard gold futures contracts (ticker: GC) take the seventh place in liquidity and the second one among the commodity futures giving way only to the crude oil futures.

The second part of the article about gold futures will be published soon. We will consider in it dependence of the gold price on the USD exchange rate and find out why the gold ‘paper’ and physical markets of this precious metal are parallel universes.