The earliest mention of a futures operation can be found in Politics by Aristotle, written as early as in 335-322 BC. Aristotle narrates a story about a wise man from Miletus named Thales who pulled a clever trick.

Based on his own astrological observations Thales made a conclusion that the olive crop would be high and he reserved all oil mills in Miletus and neighboring Chios for the spring at a bargain price. The forecast proved true and the demand on oil mills was high. Thales farmed out the oil mill services on beneficial terms and became rich.

In this article:

- a futures and futures trades – what is it?

- how to trade futures on a modern exchange;

- how to increase gains from futures contracts trading with the help of software.

SO, WHAT IS A FUTURES?

The future is the time to come. and futures is a contract for buying/selling an underlying asset on a certain date in future, however, at the current market price.The underlying assets are stock, bonds, commodities, currency, interest rates, inflation level, weather, etc. (You can find more information about a diversity of futures contracts in the Top Six Unusual Futures article).

The exchange platforms, where futures are traded, are called forward markets. The main reason of emergence of the forward trading were problems with delivery of goods. In order to reduce risks connected with roads, weather and storage of goods, forward contracts with settlements and delivery in future were introduced into practice.

In 1865, the Chicago Board of Trade developed, for the first time, standard framework agreements on grain trading, which were called futures contracts. The contracts were standardizes by quality, quantity, periods and places of delivery of the commodity, by which a deal is made. At the same time, the system of futures margins was introduced. The traders made cash contributions into the exchange fund. Due to this system, the buyers and sellers were protected from unfair practices of each other.

- a name. For example, a futures on the RTS index is called RTS-12.18;

- a ticker. For example, a futures on the RTS index with the date of expiration in December 2018 has the RIZ8 ticker. We will speak about ticker decoding a bit later;

- a contract type (settlement/deliverable). We will speak about types in more detail also a bit later;

- a size (a number of units of an underlying asset for one futures);

- a period of circulation;

- a date of delivery;

- a minimum price change (increment);

- a minimum increment value. For example, it is RUB 13.24 for a futures on the RTS index.

Complete information on the futures contracts specifications is available on the web site of an exchange, which provides access to the futures trading. For example, these are links to the futures specifications of the Moscow Exchange and CME. A futures contract ticker consists of 4 symbols.

- Fist two symbols specify the underlying asset (RI is the RTS Index, CC is cocoa, ZC is corn, CL is crude oil, 6E is EUR/USD and so on). Usually these symbols are the same for the same underlying assets on different exchanges. However, there could be differences, since each exchange has the right to set its own code for an underlying asset. For example, BR on the Moscow Exchange means a Brent oil futures contract, while BR on CME means a BRL to USD exchange rate futures.

- The third symbol is the month of expiration of a futures contract. The following symbols are accepted in the world practice: January – F, February – G, March – H, April – J, May – K, June – M, July – N, August – Q, September – U, October – V, November – X and December – Z.

- The fourth symbol is the year.

For example, the GZU8 futures contract code means a futures on the Gazprom (GZ in the code) stock with the term of delivery in September 2018 (U is September and 8 is 2018). RIZ8 is a futures contract on the RTS index with expiration in December 2018.

Deliverable and settlement futures

A futures contract cannot be just canceled or, according to the exchange terminology, liquidated. If a contract is made, it can be closed either by the way of delivery of the underlying asset (deliverable futures) or by the way of making an opposite deal for the same number of contracts (settlement futures).- Settlement futures do not envisage physical delivery of a commodity. At the moment of expiration, the exchange closes open contracts and settles the variation margin. These are contracts on oil, gold, weather, interest rates, currency and indices.

- Deliverable contracts envisage delivery of the underlying asset at the moment of the contract expiration. This could be coffee, grain or stock.

At present, only 1-3% of futures trades result in physical delivery, which testifies to a high speculative component of this market. Contract execution, that is, opining of an opposite trade for settlement futures or delivery of the underlying asset for deliverable futures, takes place at the moment of its expiration. The exchange automatically executes (carries out a reverse trade) open settlement futures contracts on the last day of their circulation.

Futures pricing.

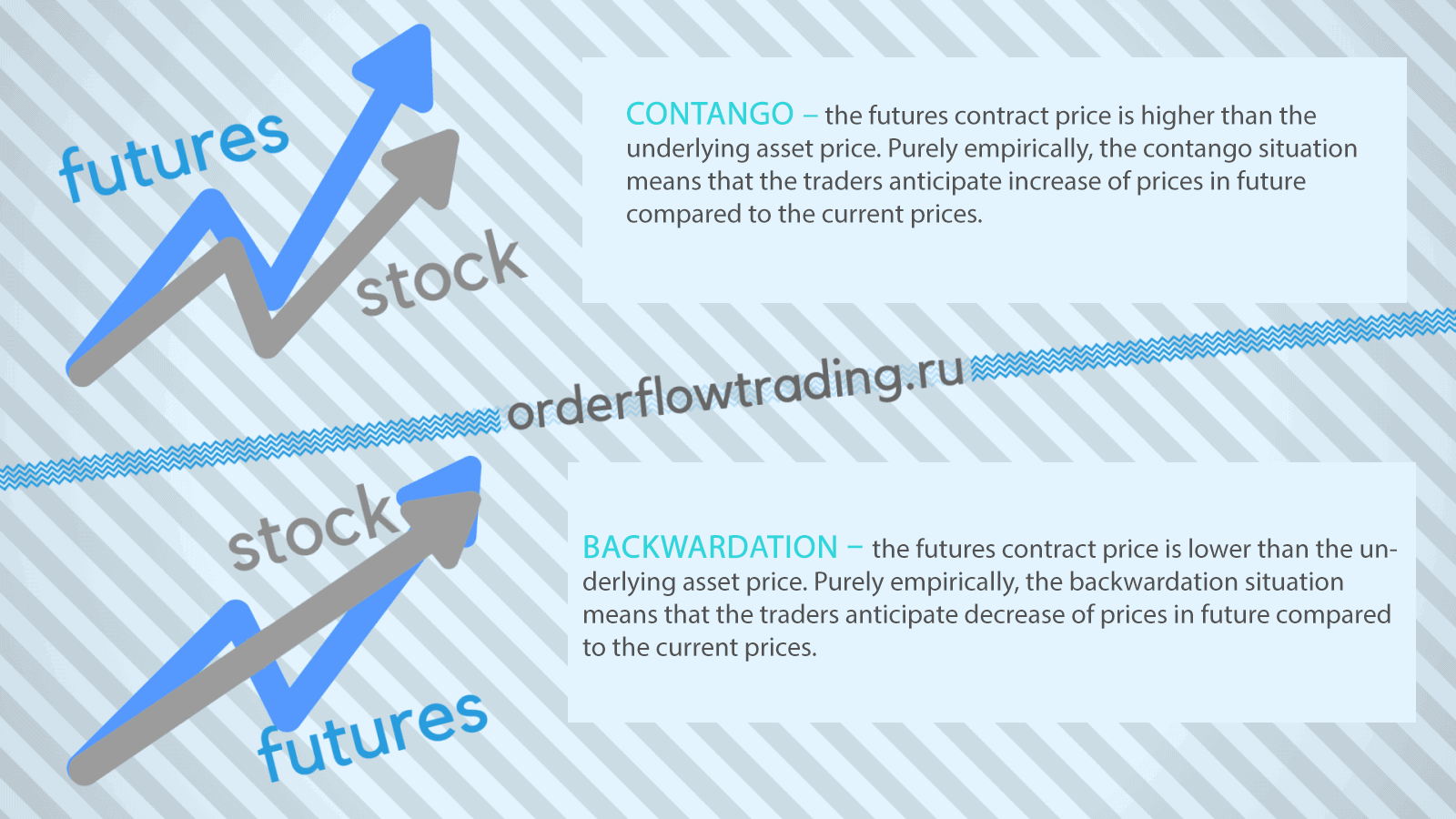

The exchange chart shows data about the course of futures trading registering all futures buying and selling trades. The price, at which the last contract was executed, is considered to be the current futures price. If a contract is still valid, its current price is ever changing. And here we face an interesting nuance. The futures contract price is always a bit different from the underlying asset price, although it has a direct correlation with it. The closer the expiration date, the smaller is the difference between the futures and the underlying asset. As regards commodity futures, there could be situations, depending on whether a futures is cheaper or more expensive than the underlying asset, which are called:- contango – the futures contract price is higher than the underlying asset price. In fact, contango is a situation of a stable market when supply completely satisfied demand and there are even significant reserves of one or another commodity. Purely empirically, the contango situation means that the traders anticipate increase of prices in future compared to the current prices;

- backwardation – the futures contract price is lower than the underlying asset price. It happens when demand significantly exceeds supply and there is no sufficient amount of a commodity or its reserves are scarce. Purely empirically, the backwardation situation means that the traders anticipate decrease of prices in future compared to the current prices.

The order of buying-selling a futures contract.

When executing a trade, both the buyer and seller of the futures contract deposit a futures margin, which is a financial provision of the contract execution.The following types of the margin are applied:

- a futures margin is deposited for each open position, changes depending on the market fluctuations and guarantees fulfillment of commitments of both a buyer and a seller;

- a variation margin is a sum of profits/losses, which are credited/debited to the trader’s account every day in the end of the trading session.

In reality, in the epoch of digital trading, execution of a futures contract can be reduced to one mouse click on the Buy or Sell button. In this article you can watch how to open trades directly from the ATAS chart.

WHY SHOULD WE BUY A FUTURES ON AN UNDERLYING ASSET TODAY IF WE CAN BUY THIS ASSET IN FUTURE?

Futures buying and selling operations depend on the aim the traders pursue:- Hedging;

- Speculation

Let us consider both cases in more detail.

Futures trading for hedging.

Hedging is the first and original purpose of a futures contract.Let us assume that you produce petrol and you are happy with the current oil price. Naturally, you would prefer to insure your business from possible fluctuations of raw material prices in future. In this case you sell an oil futures and carry on your stable business with cloudless prospects and not caring about news.

Another example. Some company, selling a real commodity with its delivery in futures at the price of the current day, simultaneously performs an opposite operation in the futures market, that is, it buys futures contracts on the same quantity of the commodity and for the same period. This company insures itself against losses. The insurance principle in this case is built in such a way that losses in one transaction result in profits in the other and vice versa. How does it look in reality? For example, Oliver Johnson, a farmer from Minnesota, expects to get a wheat yield in three months and he would deliver this wheat to a regular buyer. But there is a risk that the wheat price can go down by that time. That is why he decides to insure himself against such a disappointment through selling a futures contract by USD 3,000 per ton.

Now, two outcomes are possible for Oliver Johnson:

- The wheat price goes up to USD 4,000 per ton in three months time. Then the farmer makes profit of USD 1,000 (4,000-3,000) on selling wheat, but loses USD 1,000 (3,000-4,000) on selling the futures.

- The wheat price goes down to USD 2,000 per ton in three months time. Then the farmer loses USD 1,000 (2,000-3,000) on selling wheat, but makes profit of USD 1,000 (3,000-2,000) on selling the futures.

Futures trading for speculations.

Speculative trading of futures on an exchange promises high profits. This is why it attracts traders to the forward market. So, why is futures trading commercially profitable?Let us consider a real life example :

If we would have bought GZU8 (a futures on the Gazprom stock) at the price of RUB 13,050 per contract on June 22, 2018, then we would have fixed the price of RUB 130.5 (one futures contract of GZ implies delivery of 100 shares) per one Gazprom share. At the moment of expiration (termination of validity) of the contract on September 20, 2018, the futures price was RUB 16,000, that is, the price of one share was RUB 160 (16,000/100). Doing so, the trader either would have received profit of RUB 29.5 (160-130.5) per one share or would have had the right to buy the Gazprom shares at the price of RUB 130.5 instead of RUB 160.

A natural question arises: maybe he should have bought the stock on June 22 and not futures?

Here the speculative nature of futures, allowing a dramatic increase of profit, comes to surface.

8 ADVANTAGES OF FUTURES CONTRACTS TRADING.

Increased profitability.

Let us calculate the annual gain of the Gazprom stock and futures on the Gazprom stock without including commission fees.- Stock: buying by RUB 135 and selling by RUB 158. RUB 135,000 was invested for 90 days;

Gain in RUB is 158*1,000-135*1,000=RUB 23,000.

Annual gain is 23,000/135,000*365/90*100=69%.

- Futures: buying at RUB 13,050 and selling by RUB 16,000. RUB 30,000 was invested for 90 days;

Gain in RUB is 16,000*10-13,050*10=29,500. Annual gain is 29,500/30,000*365/90*100=398%. Consequently, when trading GZ futures a trader increases the profit from the growth of the GAZP stock in 5-10 times.

Low threshold of entering the market.

It is not necessary to pay the whole price of the futures in order to buy it. It is sufficient to deposit 8-10% only, a so-called guarantee collateral. In our example above, minimum RUB 135,000 should have been paid for acquisition of 1,000 shares of Gazprom on June 22, 2018, and about RUB 30,000 should have been deposited for acquisition of 10 futures on the Gazprom stock.Low commission fees.

The exchange commission fee for a futures on the Gazprom stock is about RUB 1 and the brokerage fee is about the same. Commission fees for stock trading are much higher and are calculated depending on the money turnover. Also, you have to pay the depositary for keeping records of your securities.By the way, the commission fees can be adjusted in the trading system ATAS in such a way, so that to control these expenditures in the real time mode.

Big credit leverage.

Many brokers offer a credit leverage of up to 1:250 for intraday trading. Thus, having only USD 2,000 on your account you can trade within a day for the amount of up to USD 500,000.High liquidity

High liquidity for popular futures, that is, a possibility to sell and buy it immediately. For example, a standard daily turnover of the USD/RUB exchange rate futures exceeds RUB 100 billion.A vast number of instruments.

More than 90 futures are traded on CME and 50 of them are on the world currencies. The Chicago Mercantile Exchange (CME) is the main world platform for trading futures. The main platform for trading futures in Russia is the Moscow Exchange (MOEX). It offers more than 40 types of futures.Extended trading time.

On the Moscow Exchange, you can trade futures from 10:00 until 23:50, that is, both in the European and American sessions.“A game” with a zero sum.

A number of sellers is always equal to a number of buyers in the futures market. Futures contracts do not appear from nowhere. To buy a futures contract one trader needs another trader who will sell it. That is why the open interest indicator, which shows a number of active contracts, is available for futures. Analysis of this indicator (it is a topic for an individual article) allows increasing the probability of correct entering into the market.Reducing the risk of speculation in the futures market

It is natural that trading in financial markets is connected with high risk. And the futures trading is not an exception. However, futures provide a unique speculation method for those who want to make less risky profits. This method is the futures spread trading.The futures spread trading is simultaneous buying and selling various futures contracts on one and the same commodity or on a commodity that is connected with it.

For example, here we will see how to trade a spread between common stock and preferred stock of Sberbank.

How to increase profit trading futures.

In order to increase trading efficiency, apply cluster analysis for better understanding of the current nature of the futures market.The cluster analysis is the most modern type of analysis, which allows comprehensive assessment of the price and volume interaction. The trading and analytical ATAS platform provides all possible instruments for the cluster analysis, including some unique developments.

Working in ATAS, a trader receives a wonderful possibility to assess the market through a microscope at any angle, using

- 25 types of footprints;

- 58 indicators, including unique developments;

- various chart types, such as Range, Reversal, Reno and others.

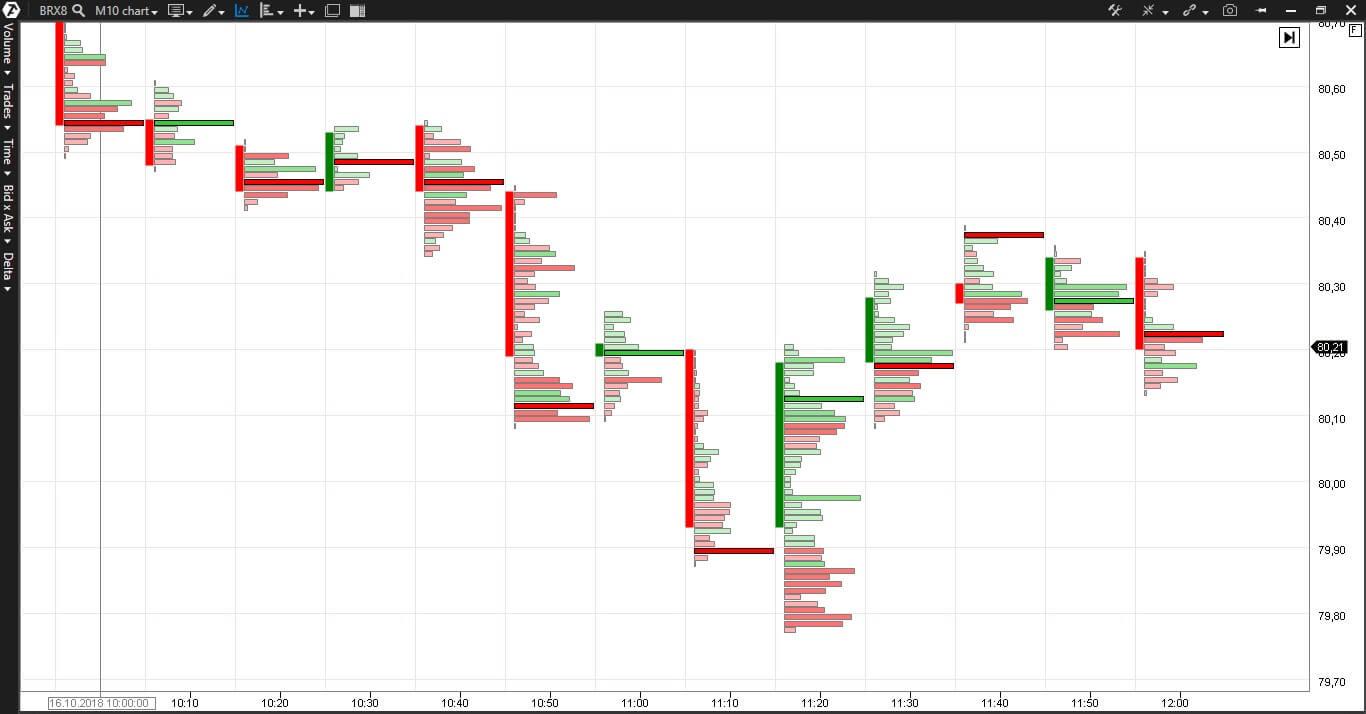

Example

Picture presents a cluster chart (or a footprint) of the BRX8 oil futures.