- Contango is a price premium.

- Backwardation is a price lagging.

These concepts are applied only for the futures markets. In order to explain the idea, we will have to dig a bit into the theory and mathematical formulas.

The concept idea. Theory

Futures contracts were developed for hedging risks, connected with underlying assets. That is why, as a rule, the futures and spot prices are not equal but connected with each other by the following formula:

F = S * ert

where:

- S – asset spot price,

- r – risk-free rate,

- t – time until the contract expiry,

- e – exponent.

In simple words it means that a trader should receive income for owning a futures. This income shouldn’t be lower than alternative risk-free variants – for example, deposits.

This formula doesn’t take into account expenditures on the commodity physical storage. However, if we consider commodity futures with a possibility of physical delivery (for example, on oil, metals, agricultural crops, etc.), then additional expenditures on physical storage should be taken into account. In such a case, the previous formula will change:

F = S * e(r+u)*t

where: U – annual storage cost

If the futures price coincides with the theoretical one (calculated by the formula), this market state is called ‘full carry’. In reality it means that the futures price takes into account all expenditures – the financial ones and those that are connected with storage.

However, in reality the futures price is often above or below the spot price. In such a case, the formula is supplemented with one more indicator – ‘convenience yield’ Y.

F = S * e(r+u-y)*t

In fact, the ‘convenience yield’ is the benefit of physical ownership of a commodity in the spot market. This concept is applied only for commodity markets, because there could be a deficit or overabundance of physical commodities in them. Convenience yield couldn’t be applied to the financial markets because there cannot be a deficit of stock indices in them.

For example, it becomes very cold at the end of the winter, when fuel reserves are nearly exhausted. If it happens, the prices on the heating fuel or black oil fuel sharply grow. At such moments, it is more profitable to keep fuel in storages than to have futures on it.

Another example – if the summer is rainy and cold, some part of crops, for example, wheat, could be lost. If the physical amount of wheat decreases, there is a deficit of wheat and its price grows. In such a case it is also good to have wheat reserves in a storage.

What contango and backwardation are

Now, we have approached the contango and backwardation concepts in simple words.If all overhead expenditures are above the convenience yield, the commodity market will be in the contango state. In this event, the futures market takes full account of the storage expenditures and it is profitable for traders to sell a commodity in the future rather than right now. In the contango state, traders wait for the price growth that is why contracts with the nearest months of delivery are traded cheaper than more distant contracts.

Contango is the market state when futures prices exceed spot prices.

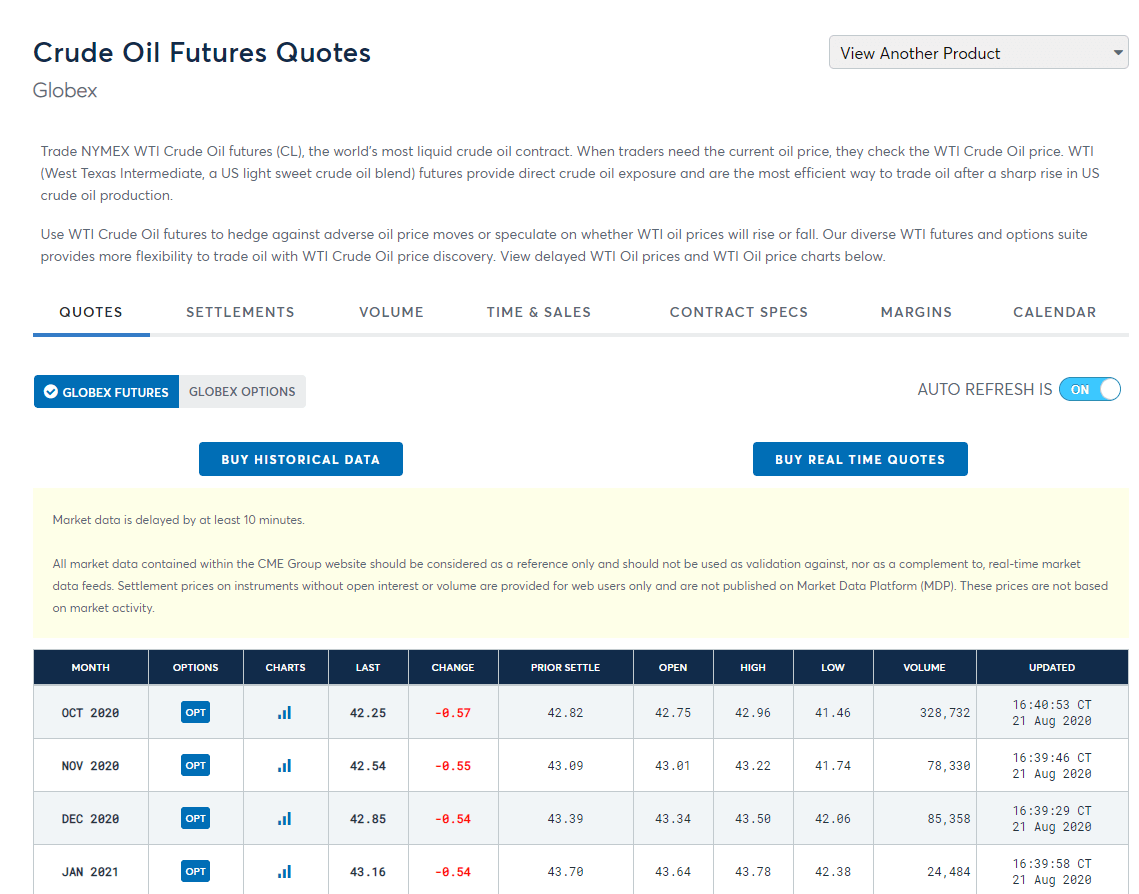

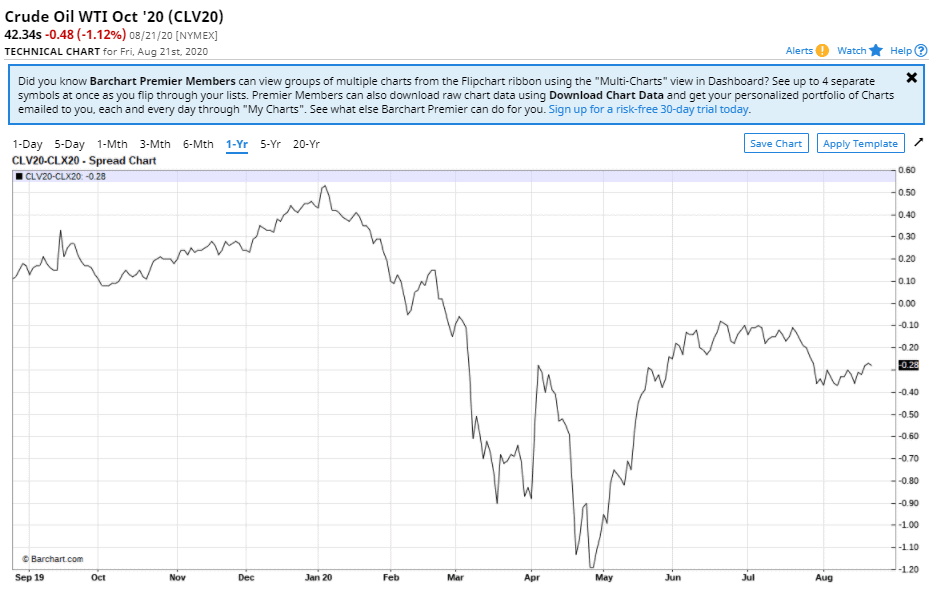

For example, the oil market is in the contango state now because the contracts with more distant terms of delivery are more expensive than the current contract. See Picture 1.

Backwardation is such a market state when spot prices exceed futures prices.

What the basis is

Markets stay in the contango state more often, that is the futures contracts are more expensive than their underlying assets. It is connected with the fact that you need less money for buying a futures than for buying its underlying asset. The difference between the guarantee collateral and the underlying asset value could be invested and it may bring additional yield. That is why, if terms are equal, it is more profitable to buy the futures contracts than the underlying asset.The difference between the futures price and asset price is called the basis.

The basis could be both negative and positive. The closer the futures contract to the date of expiration, the less the basis is.

Is it possible to make money on contango?

The contango and backwardation concepts are used when working with calendar spreads and in arbitrage operations. Significant deviations of spreads from historical values show that there is an obvious disbalance in the market. As a rule, disbalances do not last long and the market comes back to the neutral state. However, there could be exceptions and we will speak about them a bit later.Let’s consider an example of working with the calendar spread of the RTS index futures. We built the RIU0/RIZ0 spread chart. The third ATAS version had spread charts. They will become available in the 5th ATAS version very soon.

In our example spread = RIU0 price – RIZ0 price, which means:

Spread = the current futures (the date of expiration – September 17, 2020) price minus the next futures (the date of expiration – December 17, 2020) price. See Picture 2.

In order to sell or buy a spread, it is necessary to open two opposite trades simultaneously with the nearest and next contract. Such trades are called a calendar spread and it is one of the arbitrage trading types.

If the spread value is too low with respect to historical data, an arbitrageur buys the nearest contract and sells the distant one. If the spread value is too high, he does it the other way round – sells the nearest contract and buys the distant one.

It is believed that risks are lower in such a strategy than if only one contract type is traded. Moreover, some exchanges take lower guarantee collateral for double trades, because they perceive them as a spread rather than trading individual futures. See Picture 3.

| Date | RIU0 | RIZ0 | Total spread profit |

| June 25, 2020 – entry | buy 123060 | sell 121990 | |

| June 26, 2020 – exit | sell 121940 | buy 120260 | |

| Total | -1120 | +1730 | +610 |

Contango, backwardation and oil

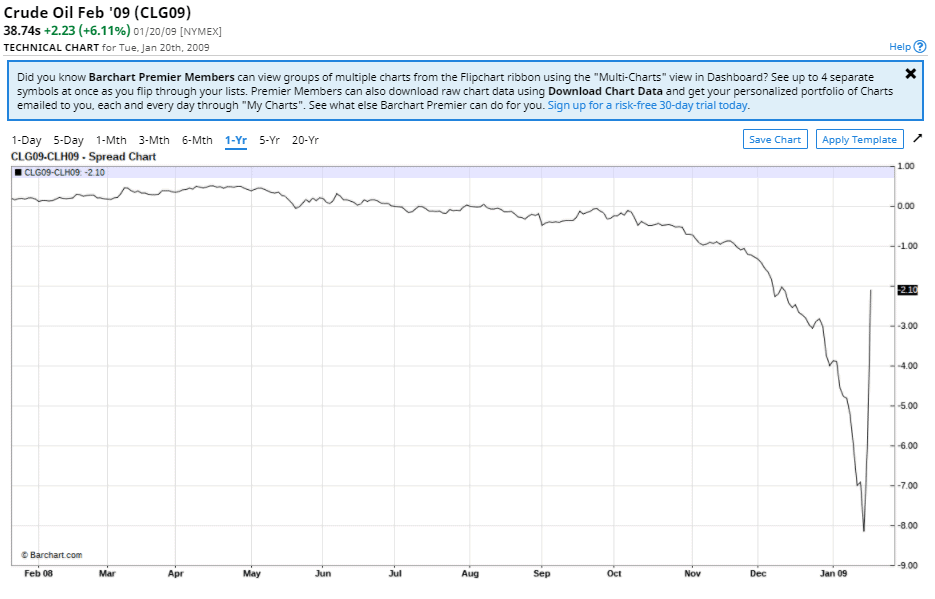

We want to remind you that the negative basis emerges in the contango state, while the positive basis emerges in the backwardation state.The oil market example. In 2009, the calendar spread between the nearest contracts expanded to wild values and there were ‘wild contango’ situations, which lasted for several months. For example, in 2009, the calendar spread between the February and March contracts expanded to USD 8, although during the period from 1997 to 2008 the calendar spread stayed within the range from USD -2 to USD +2. See Picture 4.

Theory and practice

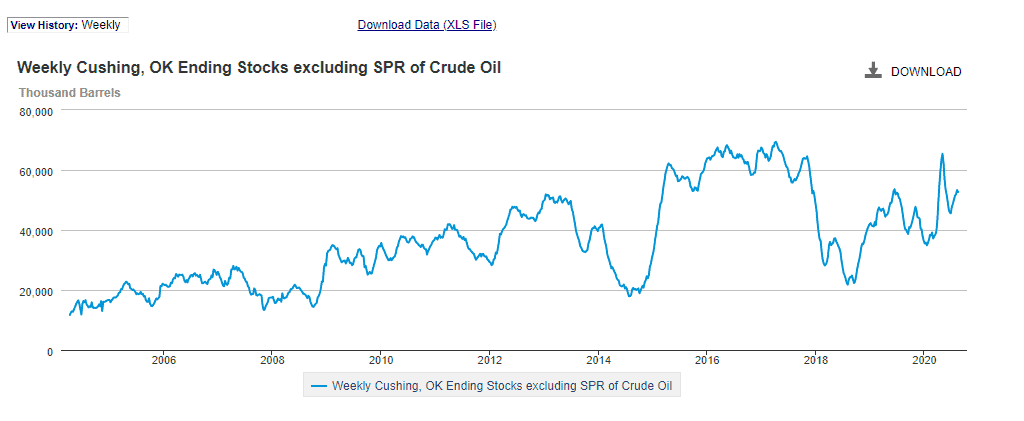

Theoretical growth of the oil volume in storages should lead to the price decrease and contango state. The lower the prices, the more oil the traders want to keep in storages. Due to this, the contango state becomes stronger.The price change in practice could be connected with speculative actions of traders. You can check weekly data of crude oil reserves in the Cushing storage facility on the web-site of EIA independent American agency. See Picture 5.

In order to work with spreads, it is necessary to analyse historical data and control risks. Initial margin on the oil spread will be significantly lower than the margin on two separate contracts. However, margin requirements may aggressively change during a trading session depending on volatility. See Picture 6.

Summary

- Contango is the market state when futures prices exceed spot prices.

- Backwardation is the market state when spot prices exceed futures prices.

- The difference between the futures price and asset price is called the basis.

Information in this article cannot be perceived as a call for investing or buying/selling of any asset on the exchange. All situations, discussed in the article, are provided with the purpose of getting acquainted with the functionality and advantages of the ATAS platform.